FTSE 100 FINISH LINE 30/4/26

FTSE 100 FINISH LINE 30/4/26

On Thursday, London’s stock market showed signs of resilience, with the FTSE 100 climbing over 1.5%. Robust earnings reports and strong commodity prices drove this uptick, overshadowing the cautious sentiment ahead of the Bank of England's upcoming decision. While the atmosphere appeared more optimistic than in previous days, it still lacked the fervour of a full-blown domestic risk rally. The leading sectors in the FTSE were primarily global industrials, mining companies, and precious metals, all of which thrived amid ongoing concerns about the U.S.-Iran conflict, oil prices soaring above $122 a barrel, and the potential for another energy crisis that could compel central banks to maintain restrictive policies for an extended period.

The performance of individual stocks played a significant role in lifting the indices. Rolls-Royce saw a remarkable surge of nearly 6.8% after it reaffirmed its profit outlook, delivering exactly what investors were hoping for: clarity, execution, and confidence in a high-quality industrial turnaround. Glencore also benefited, rising 2% following a 19% increase in its first-quarter copper production, which bolstered support for mining stocks as investors sought exposure to tangible assets. Precious metals stocks experienced a resurgence as inflation hedging gained traction, with Endeavour Mining climbing 6.2% and Hochschild gaining 5.1% as gold prices rallied. However, not all stocks fared well; Weir Group fell by 7.5% after disappointing first-quarter orders, serving as a reminder that investors remain quick to react to any signs of weakening demand. The takeaway from these stock movements was unmistakable: credibility in guidance and leverage to commodity prices are being rewarded, while uncertainty in cyclical trends is not.

Meanwhile, the Bank of England opted for a cautious approach, maintaining the Bank Rate at 3.75% with an 8-1 vote, where Huw Pill stood out as the sole member advocating for an increase to 4.0%. While this decision was largely anticipated, the nuances were significant: the Monetary Policy Committee explicitly highlighted the Iran conflict as a pressing risk to inflation and growth, noting that escalating energy disruptions could necessitate higher borrowing costs in the future. The British pound remained relatively stable, while two-year gilt yields dipped by about 5 basis points, indicating that markets found some reassurance in the decision but were still wary of a potential hawkish surprise down the line. Politically, the ongoing controversy surrounding Keir Starmer's appointment of Peter Mandelson as U.S. ambassador added a layer of complexity, further dampening the UK's risk appeal at a time when the FTSE is already trailing behind its European and U.S. counterparts. In summary, Thursday’s market bounce was tangible but was chiefly fuelled by strong earnings and commodity performance rather than renewed faith in the UK’s economic narrative.

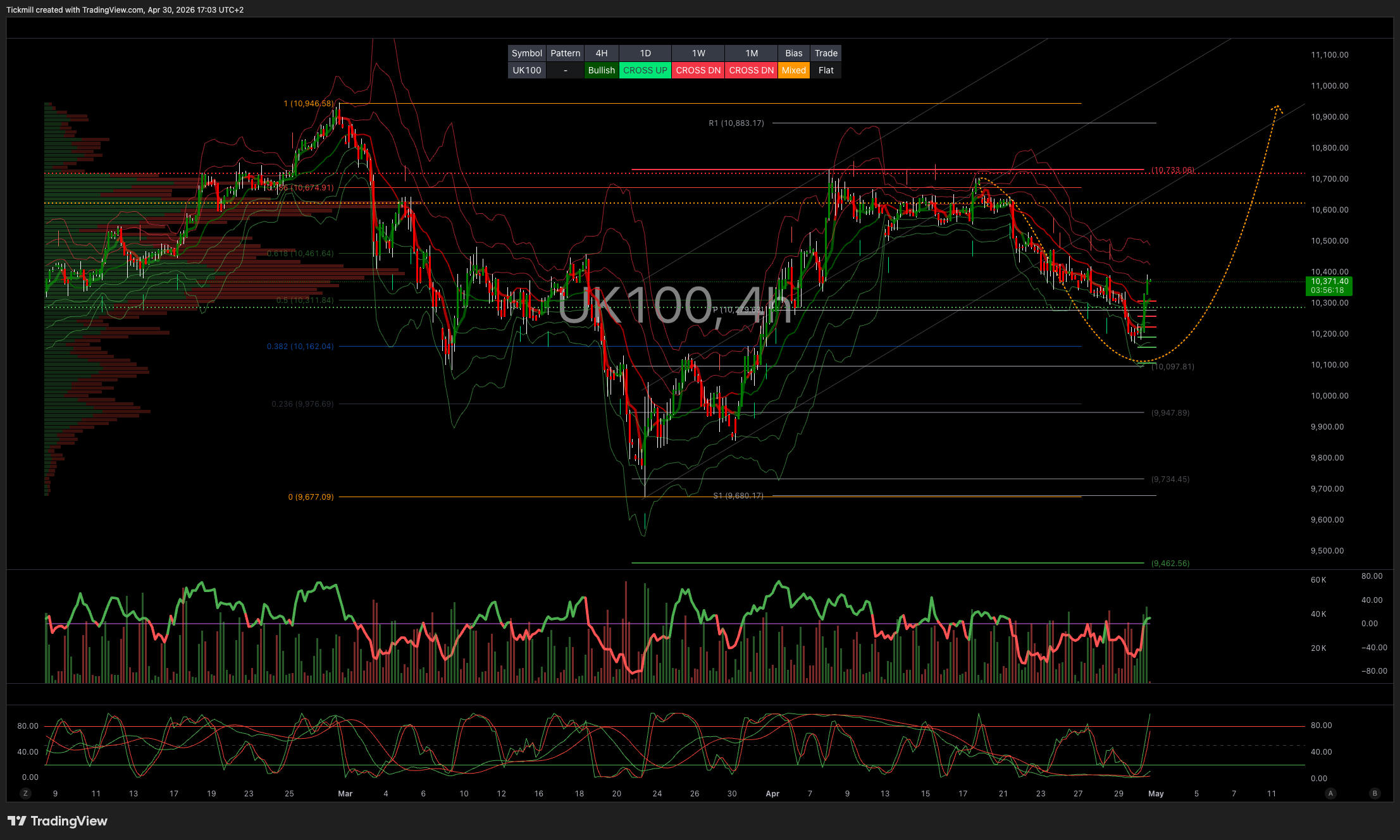

TECHNICAL & TRADE VIEW – FTSE100

Daily VWAP Bearish

Weekly VWAP Bullish

Above 10100 Target 11000

Below 10000 Target 9469

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!